ESR-REIT

Cambridge REIT to watch out for

Post Reply

1-20 of 20

Post Reply

1-20 of 20

hi freeme the private placement 71 million is issue to who.? or to insitutional buyer. any idea?

freeme ( Date: 27-Jul-2009 20:28) Posted:

halt today due to placement at 0.395.. 5% discount of last closed px.. Hope it will be well receive to shareholders!

|

|

halt today due to placement at 0.395.. 5% discount of last closed px.. Hope it will be well receive to shareholders!

Dividend Discount Model-derived target price raised to S$0.48 (from S$0.47). We maintain our estimates but use a lower discount rate of 9.4% (from 9.6%) based on a lower risk free rate of 4.8% applied across our REIT universe.

Cambridge Industrial Trust remains the cheapest industrial REIT under our coverage. Price/Book Value has risen to 0.5x, but still lags behind the REIT sectors 0.6x average. We believe there is room for price upside.

http://www.nextinsight.com.sg/content/view/1350/60/

CIT reports 4.2% growth on DPU for the second quarter of

2009

Highlights:

Portfolio occupancy remains high at 99.5%, an increase of 0.3% Q-o-Q

Stability of revenue

DPU increased to 1.345 cents, representing a 4.2% increase Q-o-Q

Net Asset Value (NAV) per unit decreased to S$0.62 following portfolio

revaluation decrease of 9%

Asset divestment program progressing

Current yield is abt 13% p.a.. one of the highest paying S reits.

Jus Vested

Business Times - 02 Feb 2009

Cambridge Ind'l Trust reports 4% fall in DPU

It hopes to deliver stable DPU this year with its long average lease expiry

CAMBRIDGE Industrial Trust (CIT) has announced a distribution of 1.373 cents per unit for the quarter ended Dec 31, 2008, said Reit manager Cambridge Industrial Trust Management Ltd (CITM).

The Q42008 DPU is 0.117 cent lower than the same period a year ago.

CIT's total net distributable income for FY2008 was $47.9 million with an annual DPU of 6.012 cents. This represents an annual yield of 21.9 per cent based on the closing price of $0.275 per unit on Dec 31, 2008, said CITM.

The annual DPU for FY2008 of 6.012 cents was a decrease of 4.0 per cent from 6.262 cents in FY2007.

Said Chris Calvert, chief executive officer of CITM: 'We are pleased to report a set of consistent results for FY2008 in this difficult economic environment.'

All its properties are signed with long leases of up to 15 years, with fixed rental escalation. The weighted average remaining lease term of CIT's existing portfolio of 43 properties remained stable at 5.7 years as at December 2008, CIT said.

As at the end of 2008, CIT has a portfolio of 43 properties with 653,673.39 square metres of lettable area valued at $995.4 million. The weighted average land lease on these properties is 39.4 years, excluding freehold property which comprises 5.4 per cent of total lettable area. About 35 per cent of the portfolio of properties is in the logistics and warehousing sector, with the next significant segment in the light industrial space accounting for 34 per cent.

The occupancy of CIT's portfolio was 99.5 per cent.

'CIT continues to place prudent capital management at the centre of its business strategy as evidenced by recent signing of term sheets with three banks under which they will commit to provide a $390 million syndicated term loan,' it said. The group's gearing was 37.8 per cent, below its long-term leverage target of 40 per cent.

CIT said its future outlook will be determined by the severity of the impact of the current financial crisis. 'However, for this financial year, CIT believes itself to be well-positioned to deliver stable DPU, with its relatively long average lease expiry of 5.7 years on top of a high 16-month security deposit,' it added.

|

The company announced that they were going to release the year's results on 30jan but got no news yet. Wonder why the delay

Thanks for the info!

Share market always recovery early !!

crimson ( Date: 05-Jan-2009 10:16) Posted:

Any experts can provide a FA for this counter please?

Btw, why is it that recent weeks lots of property counter are going up, even though the property price are all expected to fall in the coming quater(s), anyone able to give some insights/guesses?

|

|

Established with objective of investing in real estate assets used mainly for industrial purposes.

Jul 08, co is in the process of becoming a Shariah-compliant Reit, so as to tap the growing pool of M-East capital.

Mar 08, co inked agmt to acq Natural Cool Hldgs new hdq at Tai Seng Street for 55.2m. Feb08, Oxley Grp acq 20% stake in Cambridge Industrial Trt Mgt the manager of co thru the purchase of 33% stake in CB Real EstateInvs Mgt. co portfolio of 40 ppts is valued at 927.8m as at Dec 07.

co entered into agmt with Tellus Marince Engr to acq 21B Senoko Loop for 14.67m. The co manager CB IND Trt Mgt is a JV bet CWT n Mitsui. As Mitsui is a shareholder of hte co, mgt believes that it will contribute its expertise gained in managing Japan's first Reit n will assist the co in seeking oppr for acqn fr its biz n/w. Listed on 2500706 0.68 apiece.

3QTR, turnover soared 45.8% to 53m. co will pursue its current strategy of prudent capital mgt n active asset mgt to optimise d performance of portfolio.

2H07 was on 290108. 1H08 div 0.03149cts, 3 QTR 0.0149.

Generally, STI moves, other counters will join the ride as well.

crimson ( Date: 05-Jan-2009 10:16) Posted:

Any experts can provide a FA for this counter please?

Btw, why is it that recent weeks lots of property counter are going up, even though the property price are all expected to fall in the coming quater(s), anyone able to give some insights/guesses?

|

|

Any experts can provide a FA for this counter please?

Btw, why is it that recent weeks lots of property counter are going up, even though the property price are all expected to fall in the coming quater(s), anyone able to give some insights/guesses?

jp morgan - overweight.

uobkayhian - buy

nomura - neutral

www.nextinsight.com.sg has a report on these analysts. wonder why the nomura analyst not liking the 25% yield ????

If interest in reit and trust...i personnally like hyfluxwatert, Parkwaylife, and First reit..no a call to buy...but do take a look closely..vested till fundamental change for me to sell.

Actually, to cal the yield is misleading...because they are cal base on current share price and the latest distribution given out..

I think the yield should be base on our own individual buying px with the latest distribution..but that both are subject to change into the future,

Buying base on dividend is not so good as buying the counter for it growth and prospect...value investing.

Just my opinion..pls dont take it hard.

Yup, also changed CEO to a Chris Calvert.

Googled his background: From Mar 2008 to Nov 2008, Calvert was CEO of Blaxland Funds (Asia).

Prior to that from Jan 2007 to Mar 2008, he was CEO (Asia) of

MacarthurCook. He was head of property for MacarthurCook from Jul 2003

to Dec 2006.

Source: http://www.theedgesingapore.com/index.php?option=com_content&view=article&id=1143:chris-calvert-replaces-ang-poh-seng-as-ceo-of-cambridge-industrial-trust&catid=931:business-2008&Itemid=53

Noticed too that the volume traded on day of announcement was also quite high. Hopefully price may pick up from here

It is confirmed - Cambridge will refinance approx 390m worth of debts at 6.6 % interest (including amortisation of upfront cost for a fixed period of 3 years.

THe impact on their dividend will be 0.9 cents per share per annum. This means that based on the current projected dividend of approx 6 cents per share, their dividend will drop to approx 5 cents per share, per annum, or 1.25 cents per quarter.

Ay current price of 20 cents, the dividend yield is 25 % per annum.

With the financing risks removed, the only risk remaining would be early termination by current tenants. (Do your own research on the existing tenants)

According to a recent UBS report on reits in Australia and Spore, when the financing risk for reits in Asutralia was removed, via re-capitalising, etc, the stocks rallied up quite strongly subsequently, as compared to those reits who faced uncertain refinancing options.

Not a call to buy/sell. Investors should do their own homework.

there is a Kim Eng Securities table that projects a 8% fall in DPU next year. doesnt look bad considering that the 2009 will still be 27%!!!!

http://www.nextinsight.com.sg/content/view/737/60/Cambridge and other Reits have collapsed, i can't believe that the market has swung to such a risk-averse mindset.

In a UBS report on Spore Reits, dated 09th Dec, the analyst noted 'positive press commentary on a potential pending successful refinance by Cambridge Reit in Finance Asia (5th Dec).

THe press comments are ' Cambridge S$385m three-yr term loan refinancing is currently in documentation via mandated lead arranger HSBC, the fundraising has been well received and oversubscribed, but the deal size is not increased as this is a structured, rated asset-based financing, where the size is constrained by restriction imposed by intl rating agency. The latter are expected to rate 85 % of the loan as 'AAA' and the remaining 15 % 'AA'. Signing is expected to tale place by end of 2008 or early next yr.

Thanks to a fellow blogger by the nick of Cheng ( you can read his

blog Here) who mentioned a

red flag about Cambridge in response to the

analysis done by our Sexy VJC Girl. This culminated into this article . We took a look at Cambridge to see what the hoo ha ha ha ha..Santa Claus is about.

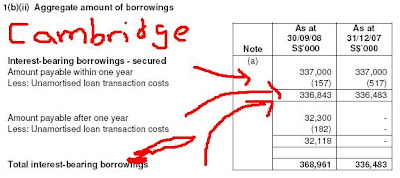

It states that they still have S$336,843,000 dollars they have to pay within a year. Wow. So, we, being extremely nosey and kaypoh like what a hot auntie would naturally be, decided to look at the footnotes to gain some perspective on this "wow" figure, and here it is:

So, really, dear investors who invested in this counter, keep your eyes peeled on any news on this. BUT, we being extremely irritating, persistent, bo liao and totally curious decided that it shan't end like that. We decided to take a look at Maple Tree Logistics which is another sort of industrial Reit. And..TAaaa DAaaaa.... No mentioning of any debt to be repaid within one year!Compare this with Cambridge.

So can islamic financing save the day for Cambridge? ( Hmm we seem to remember some article bank that Islamic financing may not be immune to the credit crisis too?........Just can't find it..)

Thanks to a fellow blogger by the nick of Cheng ( you can read his blog Here) who mentioned a red flag about Cambridge in response to the analysis done by our Sexy VJC Girl. This culminated into this article . We took a look at Cambridge to see what the hoo ha ha ha ha..Santa Claus is about.

Thanks to a fellow blogger by the nick of Cheng ( you can read his blog Here) who mentioned a red flag about Cambridge in response to the analysis done by our Sexy VJC Girl. This culminated into this article . We took a look at Cambridge to see what the hoo ha ha ha ha..Santa Claus is about.