Post Reply

1-20 of 81

Post Reply

1-20 of 81

Series of share purchases by controlling Ong family provides insider support We highlight a series of open market share acquisitions, which took place since 11 Oct, by controlling stakeholders Ong Sek Chong and his family members. During the past 41-day period, the Ong-family?s controlling stake advanced from 30.14% to 34.33%, arising from the purchase of 22.2m shares at between $0.525-0.565 apiece. Traditionally, insider purchases are viewed as having a positive signaling effect on stocks. At $0.535, Lian Beng?s valuations remain attractive at 4.3x forward P/E, compared to its closest peer Tiong Seng at 6.7x. The Ong family includes separate shareholders mainly Ong Sek Chong & Sons, Ong Pang Aik, Ong Lay Huan and Ong Lay Koon. ???

Any views on this? With current property cooling measures, i am not sure if they are affected or not.

3.1 x F14 PE dirt cheap! gd luck dyodd

Lian Beng Group

|

Ready For A Record Breaking Year |

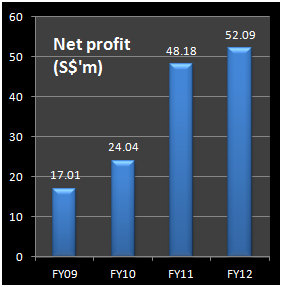

Bright outlook next year upgrade to BUY. We caught up with Lian Bengs management for updates on ongoing construction and property launches, and are now convinced that FY5/14 will be a record breaking year with earnings surpassing its 2012 peak of SGD51.4m. We are also positive that Lian Beng will be able to maintain its dividend payout of 2ct/share payable in the next quarter. We have revised our FY5/14 and FY5/15 estimates by 8-11%, and applied a higher multiple on its construction earnings. Upgrade to BUY with a revised TP of SGD0.68, indicating upside of 30.8%.

Construction orderbook at SGD1.2b. The recent Poh Lian construction scandal offered Lian Beng the opportunity to take-over the Goodwood Residence construction contract, which is scheduled for completion in October 2013. Lian Bengs orderbook currently stands at SGD1.2b including Dakota Crescent and Laurels, which if completed on schedule by end 2013, will free up manpower for further construction jobs. Since the start of 2013, Lian Beng has secured 7 private sector contracts valued at SGD739m.

New launches selling like hot cakes! King Albert Park, Hong Leong Gardens, and Hougang Plaza were launched year to date. Hougang Plaza, now The Midtown and The Midtown Residences, has achieved an average 62% take-up rate. We expect Lian Beng to begin construction at end 2013 resulting in increased contribution in the 2nd half of FY5/14. Seletar Green is expected to be launched the next quarter.

Well diversified with proven execution strength. At current levels, Lian Beng is trading at 3.1x FY14F P/E, versus peers at between 5x and 7x P/E. We peg Lian Beng construction earnings at 6x, on par with its construction peers. We like Lian Beng for (i) strong orderbook of SGD1.2b comprising of higher margin private sector projects, (ii) latest property launches with strong sell-through rates and (iii) a healthy buildup in recurrent income. We upgrade to BUY with a TP of SGD0.68. Lian Beng Group Summary Earnings Table |

FYE May (SGD m) |

2011 |

2012 |

2013F

|

2014F

|

2015F

|

Revenue |

507.3 |

445.0 |

446.9 |

593.6 |

571.0 |

EBITDA |

81.2 |

81.5 |

59.1 |

95.0 |

92.6 |

Recurring Net Profit |

48.2 |

51.5 |

40.0 |

68.5 |

66.4 |

Recurring Basic EPS (cents) |

9.1 |

9.7 |

7.5 |

12.9 |

12.5 |

EPS growth (%) |

100.4% |

6.8% |

-22.3% |

71.4% |

-3.1% |

DPS (cents) |

1.6 |

2.0 |

2.0 |

2.0 |

2.0 |

PER |

4.3 |

4.1 |

5.2 |

3.1 |

3.2 |

EV/EBITDA (x) |

3.1 |

3.0 |

6.1 |

4.4 |

4.6 |

Div Yield (%) |

4.1 |

5.1 |

5.1 |

5.1 |

5.1 |

P/BV(x) |

1.1 |

0.9 |

0.8 |

0.7 |

0.6 |

Net Gearing (%) |

-0.12 |

-0.37 |

0.17 |

0.05 |

-0.04 |

ROE (%) |

25% |

22% |

15% |

21% |

18% |

ROA (%) |

8% |

9% |

5% |

7% |

7% |

Lian Beng

Group: No Bling For Now HOLD, TP $0.49

3QFYMar13 results came in in-line with expectations. 9MFYMay13 revenue

and net profit are up 5.1% and down 24.2% YoY to SGD350.7m and SGD30.7m

respectively, due to a lack of property earnings. As we roll over our

earnings forecast to FYMay14, we have changed our valuation matrix from

P/E to SOTP valuation to value its diversified businesses.

Four construction contracts have been secured year-to-date, bringing its

orderbook to SGD986m. We view this to be positive as it surpasses our

construction orderbook estimates of SGD300m verses SGD538m contract win.

With the recent run-up in share price, we believe Lian Beng has fully

valued the incoming property earnings from M-Space @ Mandai and other

partial property stakes. Maintain HOLD.

...Prev Close: $0.490...

beng beng breakout..by UOB chart genie

Interesting movement today... pending result tomorrow or next week..

A stock is good only if ppl want to play. Look at YHM, We hldg. are they no good?

If mkt dont want to see here, good also useless.

SHARES OF Lian Beng Group have become the target of purchases by insiders in the past one year as the companys profitability continued to march upward. Read more....

Nov 23, 2012 - PropertyGuru.com.sg

By

Andrew Batt:

The number of private home sales in Singapore could drop by more than 20 percent in 2013 after spectacular increases this year.

David Neubronner, Head of Residential Project Sales for Jones Lang LaSalle (JLL), issued the warning this week, suggesting that the number of sales this year, which is expected to reach 22,000 units, will correct to more healthy levels of about 16,000 units in a worst-case scenario.

In an exclusive interview with

The PropertyGuru, he said: Put in perspective the jump this year, from 15,800 in 2011 to probably 22,000 by the end 2012, has been spectacular. We believe this is not sustainable moving forward and should correct next year."

In the worst scenario, we estimate the market to correct to the healthy levels of about 16,000 units which were achieved in 2010 and 2011. This is taking into account the anticipated economic slowdown in 2013, clampdown on residency and employment of foreigners.

Neubronner is also not ruling out a further wave of government cooling measures. He said: The possibility is always there as long as the buying continues. Based on the recent robust sales volumes and concerns of market foaming, there is always the possibility of another round of measures to take the steam out of the market.

Neubronner predicts that landed property sales will remain resilient given the limited supply and perennial demand, along with the general aspiration of Singaporeans to upgrade to a landed property. The luxury segment has seen sales volume and values declining over the past year and, according to Neubronner, should bottom out any time soon.

We anticipate a recovery next year given the values and opportunity on offer, he added.

The mass and middle market segments are expected to see most of the correcting in 2013, he said, adding that these sectors have been running up rapidly over the past year.

Neubronner also expects the proportion of foreign buyers, which now stands at roughly 20 percent, to stabilise. He said: Singapore will continue to attract foreign buying interest for a million reasons and we believe the series of measures introduced over the past years will more likely subdue the Singaporeans appetite than the foreigners.

Neubronner concluded by saying: Although sales volume will decline, we expect prices to stabilise next year. The fundamentals, like a stable economy with high employment, low interest rates, a robust leasing market in the suburban areas and the overall bullish sentiments, are still strong and we do not see these changing in 2013.

http://www.businesstimes.com.sg/breaking-news/singapore/lian-beng-oxley-and-sunview-propose-jv-20121031

Published October 31, 2012

Lian Beng, Oxley, and Sunview propose JV

LIAN Beng Group's wholly owned subsidiary Starview Investment, along with Oxley Holdings Ltd and Sunview Pte Ltd have banded together to develop an industrial land parcel in Jurong - PHOTO: CDL

The three companies have formed Ascendial Pte Ltd, taking stakes in the proportion of 51:30:19 respectively.

Ascendial won the tender for the site in Sunview Road this week with a bid of S$76.6 million.

The land parcel, zoned for Business 2 use, has a land area of about 303,251.4 sq ft and a gross plot ratio of 2.5. It has a lease tenure of 30 years.

http://sgx.i3investor.com/servlets/ptg/l03.jsp

| Last Price |

Avg Target Price |

Upside/Downside |

Price Call |

| 0.39 |

0.56 |

+0.17 (43.59%) +0.17 (43.59%) |

|

| * Average Target Price, Price Call and Upside/Downside are derived from Price Targets in the past 6 months. |

| ** Price Targets are adjusted for Bonus Issue, Shares Split & Shares Consolidation (where applicable). |

| Date |

Open Price |

Target Price |

Upside/Downside |

Price Call |

Source |

News |

| 12/10/2012 |

0.395 |

0.59 |

+0.195 (49.37%) |

BUY |

OSK |

|

| 12/10/2012 |

0.395 |

0.54 |

+0.145 (36.71%) |

BUY |

Maybank Kim Eng |

|

| 11/10/2012 |

0.39 |

0.47 |

+0.08 (20.51%) |

BUY |

OCBC |

|

| 25/09/2012 |

0.435 |

0.63 |

+0.195 (44.83%) |

BUY |

Maybank Kim Eng |

|

| 21/08/2012 |

0.41 |

0.63 |

+0.22 (53.66%) |

BUY |

Maybank Kim Eng |

|

| 27/07/2012 |

0.395 |

0.47 |

+0.075 (18.99%) |

BUY |

OCBC |

|

| 04/05/2012 |

0.39 |

0.47 |

+0.08 (20.51%) |

BUY |

OCBC |

|

| Price Target Research Article/News (past 6 months) |

| 12/10/2012 |

OSK |

Earnings dip but outlook is still good |

| 12/10/2012 |

Maybank Kim Eng |

Lian Beng Group - Still Good For the Long Haul (BUY, TP $0.54) |

| 11/10/2012 |

OCBC |

MARKET PULSE: LMIRT, SIA, Telecoms, STE, STX-OSV, Lian Beng (11 Oct 2012) |

| 25/09/2012 |

Maybank Kim Eng |

Lian Beng Group - Slew Of Launches Coming Up (BUY, TP $0.63) |

| 21/08/2012 |

Maybank Kim Eng |

Lian Beng Group - This Beng is getting bigger and better (Buy, TP SGD0.63) |

| 27/07/2012 |

OCBC |

MARKET PULSE: CMA, OSIM, Sheng Siong, Lian Beng, CDLHT (27 Jul 2012) |

| 04/05/2012 |

OCBC |

MARKET PULSE: Venture Corp, Roxy-Pacific, Hyflux, CapitaMall Trust, Lian Beng (4 May 2012) |

fyi.

lian beng current mgt is currently proposing other alternative to enhance the sharesholders' value of its wholly owned subsidiary Engineering & Machinery and 90%-owned subsidiary, Sinmix Pte Ltd ( Engineering & Concrete Business ) after it scrap the listing of them on the taiwan stock exchange. very proactive in the sense that it updates the sharesholders.

lian beng may explore ways to independently assess the market value of its Engineering and Concrete Business, just like Ezra did to Triyards Holdings Ltd.

maybank maintain buy at target price 0.53 even after the abandoned taiwan listing.

look at lian beng's ROE i believe is highest among building construction companies

But prefer lian beng due to its mgt quick ability on execution to unlock its assets value which spiral its px.......

prefer yongnam to lian beng as the former offers much more potential upside.....

but lian beng strong book orders is impressive....

no more taiwan listing... tomorrow trading will be interesting...

NextInsight Report.

Written by Sim Kih

Monday, 15 October 2012 12:00

LIAN BENGs 1Q2013 revenue (May to Aug) was lower 16.5% year-on-year at S$113.4 million as its 55%-owned industrial project M Space will be recognized only upon receipt of Temporary Occupation Permit (TOP) in FY2014. Lian Beng has sold all units of M-Space. Progressive cash collections from M-Space sales in 1Q2013 are reflected in a doubling of 'Development Properties' in the company's balance sheet to S$184.5 million (up 90.8%). The good news to look forward to in Lian Beng's property development segment: It plans to launch its 50%-owned Spottiswoode Suites and 50%-owned Hougang Plaza in FY2013. A BCA Grade A1 construction group, Lian Beng last week reported a 44.9% decrease in profit to shareholders to S$10.5 million in 1Q2013. Earnings were dampened upon adoption of the revised financial reporting standard INT FRS 115 under which revenue from industry property development can only be recognized upon receiving the TOP.

Another cause of the earnings fall was a one-off gain of S$7.9 million on the sale of an investment property in 1Q2012, which resulted in a higher base for comparison. Lian Beng's financial position as at 31 Aug:

* Cash reserves S$184.3 million.

* Construction order book: S$650 million (to be fulfilled through FY2015).

* Total borrowings increased to $209.1 million as at 31 August 2012 from $111.1 million from a year ago mainly to finance the development projects at Spottiswoode Suites and Hougang Plaza.

Lian Beng's property development segment is going to be busy. It has entered into several joint ventures which has acquired sites for redevelopment. Some of these projects include:

* Workers' dormitory at Mandai Estate

* M-Space at Mandai Estate

* Hougang Plaza

* King Albert Park

* Seletar Garden

* Hong Leong Garden Shopping Center

* Spottiswoode Suites

|

Maintain BUY with a target price of SGD0.63 pegged at 6x FYMay13 PER, backed by an attractive dividend yield of 4.7%.

Read

here.